All Categories

Featured

Table of Contents

Costs are generally reduced than entire life policies. With a degree term policy, you can choose your protection amount and the policy length. You're not secured into a contract for the rest of your life. Throughout your plan, you never have to stress regarding the costs or fatality advantage amounts changing.

And you can not squander your plan during its term, so you will not receive any financial gain from your past protection. Similar to other types of life insurance policy, the expense of a degree term plan relies on your age, coverage needs, work, way of living and wellness. Generally, you'll locate more budget-friendly protection if you're more youthful, healthier and much less dangerous to guarantee.

Because degree term costs remain the same for the duration of protection, you'll know exactly how much you'll pay each time. That can be a large assistance when budgeting your expenses. Degree term protection additionally has some flexibility, allowing you to tailor your plan with additional attributes. These typically come in the kind of riders.

You might have to satisfy details conditions and credentials for your insurer to enact this rider. In addition, there may be a waiting period of as much as six months before working. There also can be an age or time frame on the protection. You can add a youngster cyclist to your life insurance policy policy so it likewise covers your youngsters.

Tax Benefits Of Level Term Life Insurance

The fatality advantage is usually smaller sized, and protection generally lasts till your child transforms 18 or 25. This rider might be a much more economical way to aid guarantee your children are covered as cyclists can usually cover multiple dependents at when. When your youngster ages out of this insurance coverage, it might be feasible to convert the rider right into a brand-new plan.

When contrasting term versus irreversible life insurance policy, it is necessary to bear in mind there are a few various kinds. The most usual sort of long-term life insurance policy is entire life insurance coverage, however it has some key distinctions compared to degree term coverage. Here's a standard review of what to think about when comparing term vs.

Entire life insurance policy lasts for life, while term protection lasts for a certain duration. The costs for term life insurance are commonly less than whole life coverage. Nevertheless, with both, the premiums remain the exact same for the period of the policy. Whole life insurance policy has a cash value element, where a portion of the premium might expand tax-deferred for future needs.

Level Term Life Insurance

Among the major attributes of degree term coverage is that your premiums and your survivor benefit don't change. With decreasing term life insurance policy, your premiums stay the same; however, the survivor benefit amount obtains smaller with time. For instance, you might have insurance coverage that begins with a death benefit of $10,000, which can cover a home loan, and after that every year, the death advantage will certainly reduce by a collection quantity or percentage.

Due to this, it's typically a more budget-friendly sort of level term insurance coverage. You may have life insurance policy with your employer, however it may not suffice life insurance coverage for your needs. The initial action when getting a plan is establishing just how much life insurance policy you need. Take into consideration factors such as: Age Family size and ages Work condition Income Financial debt Lifestyle Expected final expenses A life insurance calculator can aid identify how much you require to begin.

After deciding on a plan, complete the application. If you're accepted, authorize the documents and pay your very first costs.

You may want to update your recipient details if you have actually had any type of significant life adjustments, such as a marriage, birth or divorce. Life insurance can in some cases feel complicated.

How can 30-year Level Term Life Insurance protect my family?

No, degree term life insurance policy does not have cash money worth. Some life insurance policy plans have a financial investment feature that permits you to build money value over time. Level term life insurance for seniors. A portion of your premium settlements is alloted and can gain interest gradually, which expands tax-deferred during the life of your protection

These plans are often considerably extra expensive than term coverage. You can: If you're 65 and your coverage has run out, for instance, you might want to acquire a brand-new 10-year level term life insurance coverage plan.

Level Term Life Insurance Vs Whole Life

You may have the ability to transform your term protection into an entire life policy that will certainly last for the remainder of your life. Numerous types of level term policies are convertible. That means, at the end of your protection, you can convert some or all of your policy to entire life coverage.

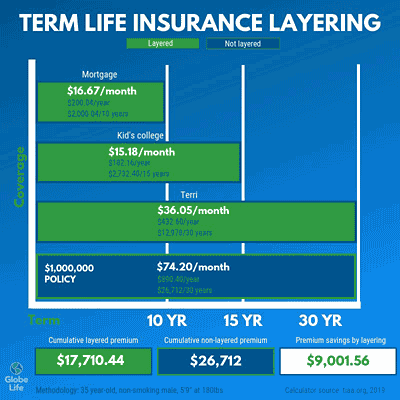

Level term life insurance is a plan that lasts a collection term normally between 10 and thirty years and features a level survivor benefit and degree costs that remain the very same for the entire time the policy holds. This indicates you'll recognize specifically just how much your settlements are and when you'll need to make them, allowing you to budget appropriately.

Degree term can be an excellent alternative if you're seeking to acquire life insurance coverage for the very first time. According to LIMRA's 2023 Insurance policy Measure Study, 30% of all grownups in the U.S. need life insurance coverage and do not have any kind of plan yet. Level term life is predictable and affordable, which makes it among one of the most popular kinds of life insurance coverage

A 30-year-old male with a similar profile can expect to pay $29 per month for the very same coverage. AgeGender$250,000 insurance coverage quantity$500,000 coverage amount$1 million protection amount20Female$15$23$34Male$19$29$4830Female$15$23$37Male$18$29$4940Female$22$35$61Male$25$43$7550Female$44$78$139Male$57$102$18860Female$108$194$355Male$149$268$500 Collapse table Methodology: Ordinary month-to-month rates are determined for male and female non-smokers in a Preferred wellness classification getting a 20-year $250,000, $500,000, or $1,000,000 term life insurance policy.

Who are the cheapest Fixed Rate Term Life Insurance providers?

Rates may vary by insurer, term, protection amount, health course, and state. Not all plans are available in all states. Rate illustration valid since 09/01/2024. It's the least expensive kind of life insurance for many people. Level term life is far more economical than a similar whole life insurance policy plan. It's easy to take care of.

It permits you to budget and plan for the future. You can quickly factor your life insurance policy into your spending plan since the costs never ever change. You can prepare for the future just as quickly because you understand specifically how much cash your liked ones will certainly obtain in the occasion of your lack.

Level Term Life Insurance Coverage

In these cases, you'll typically have to go via a new application procedure to obtain a better price. If you still need protection by the time your degree term life plan nears the expiration date, you have a few choices.

{kind=link}

Table of Contents

Latest Posts

Aig Final Expense Insurance

Funeral Burial Insurance Policy

Funeral Coverage

More

Latest Posts

Aig Final Expense Insurance

Funeral Burial Insurance Policy

Funeral Coverage